What common 401(k) pitfalls amplify hidden tax burdens?

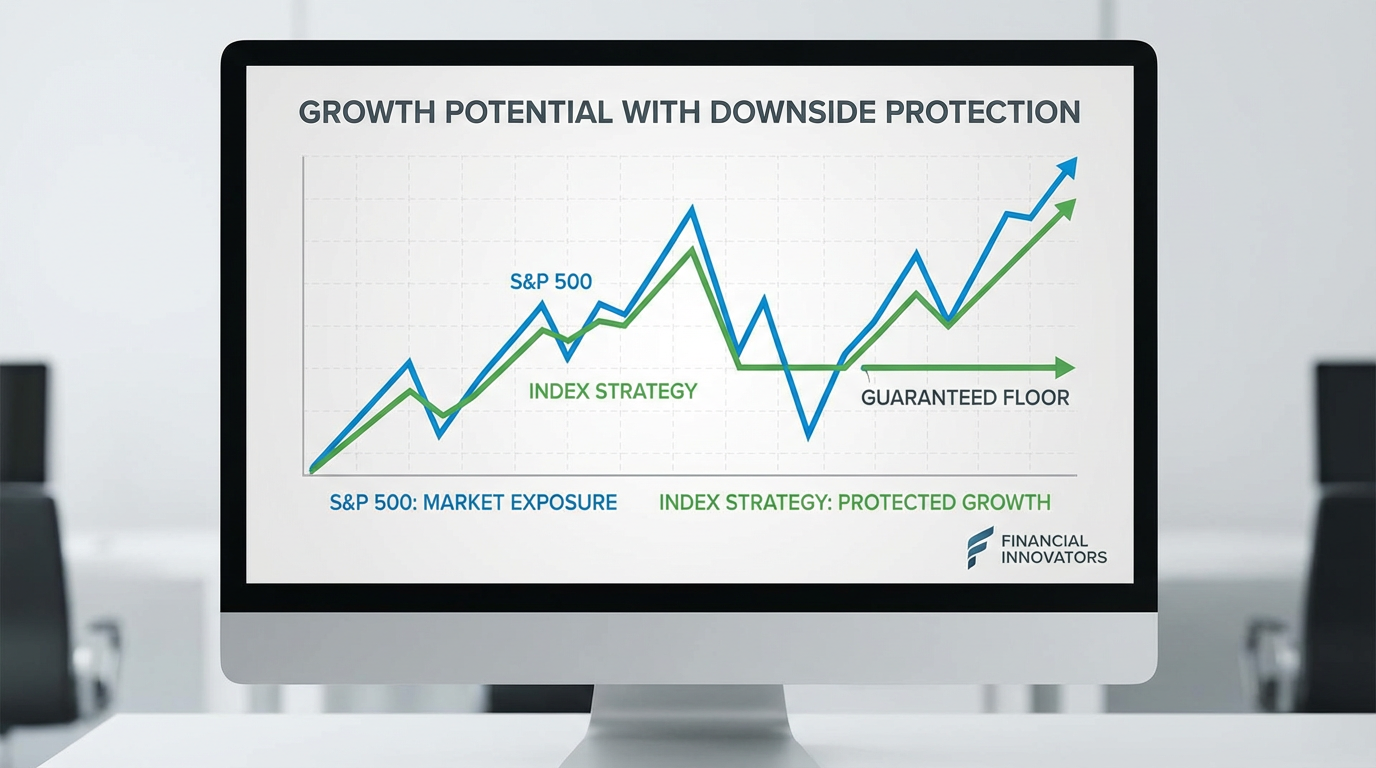

Many individuals unknowingly escalate their 401(k)'s hidden tax burdens through several common pitfalls. One significant mistake is failing to diversify tax buckets. Relying solely on a traditional 401(k) means all withdrawals in retirement will be taxed as ordinary income, potentially at higher future rates. A related pitfall is neglecting Roth conversions where appropriate; converting a portion of traditional 401(k) assets to a Roth IRA, especially during lower income years, can lock in current tax rates and create a tax-free income stream in retirement. Another common error is withdrawing funds before age 59½ without understanding the penalties and immediate tax implications, effectively eroding future retirement savings. Moreover, participants often overlook the impact of Required Minimum Distributions (RMDs) starting at age 73 (or 75 for those born in 1960 or later). These mandatory withdrawals can push individuals into higher tax brackets and increase taxes on Social Security benefits, a pitfall that better tax planning, such as qualified charitable distributions (QCDs) or Roth conversions, could mitigate. Finally, many don't leverage the potential tax benefits of certain investment strategies within their 401(k) or in conjunction with it. For instance, focusing solely on growth without considering the tax efficiency of underlying investments or failing to strategically use tools like Index Strategies, which can offer downside protection while still participating in market gains (potentially reducing the need to sell assets in downturns and incur capital gains outside of tax-deferred accounts), can lead to less effective tax management over the long term. Understanding these pitfalls is crucial for optimizing your 401(k) for maximum tax efficiency.

Ready to Build Your Financial Future?

Contact Everence Wealth for expert independent financial guidance.

Get in Touch