What 2026 IUL vs 401(k) comparison pitfalls should be avoided?

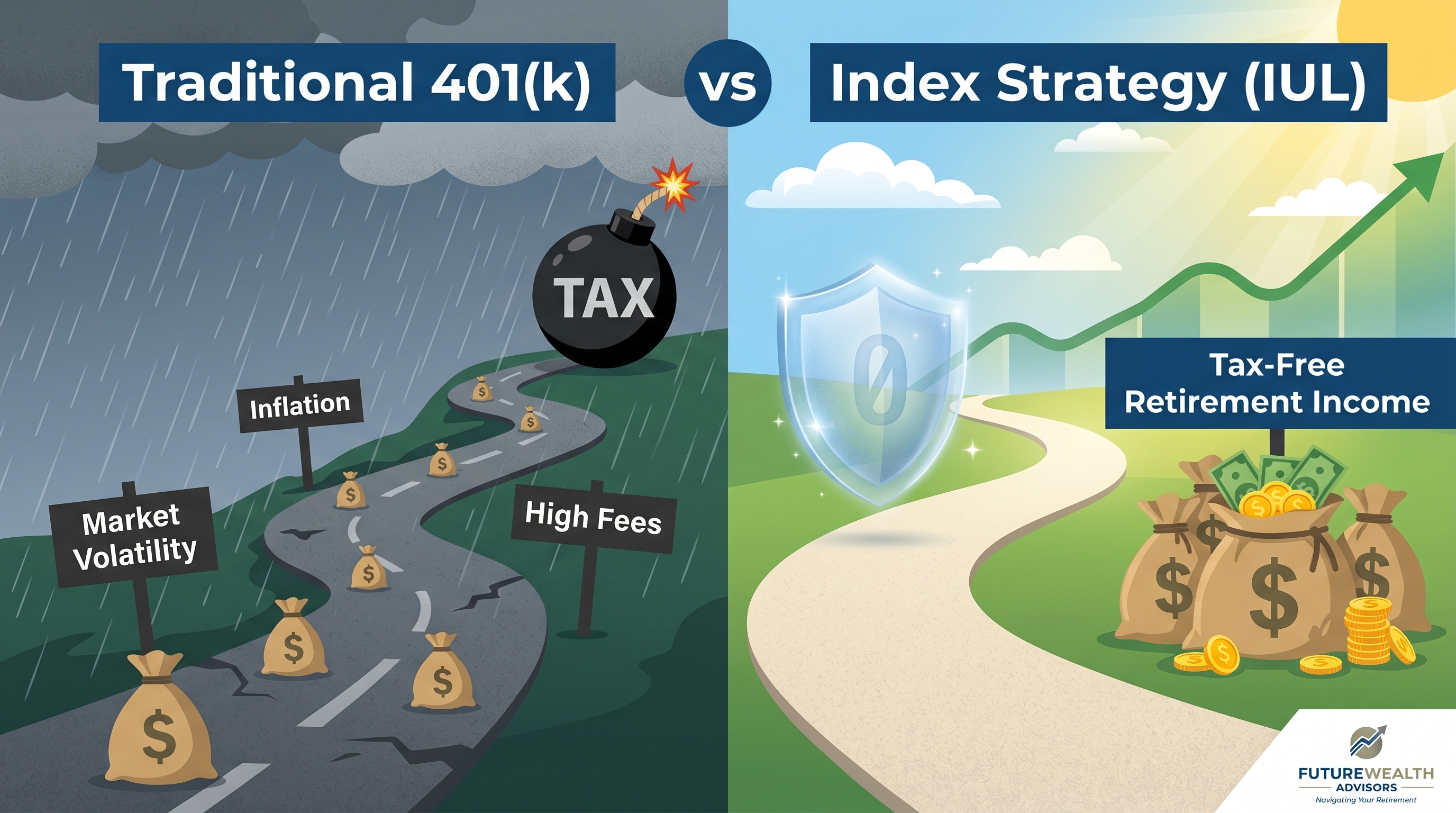

When comparing IUL vs. 401(k) for tax-free retirement wealth in 2026, a critical pitfall is failing to account for the intrinsic differences in how each vehicle generates and protects growth. Many investors mistakenly assume that the 'growth' of an IUL is directly comparable to market returns in a 401(k). However, IUL growth is typically linked to an index with caps and participation rates, offering protection against losses but also limiting upside, which can lead to lower overall accumulation if not properly understood. Another common mistake is overlooking the fee structures; while 401(k)s often have transparent expense ratios, IULs involve various charges for insurance costs, policy administration, and riders that can significantly impact net performance, especially in the early years. It's also a pitfall to focus solely on the 'tax-free' income without considering the contribution limits and liquidity. 401(k)s have specific annual contribution limits, while IUL funding is more flexible but must avoid MEC status to preserve tax advantages. Furthermore, inadequate planning for the long-term cash value growth and withdrawal strategies in an IUL can diminish its potential for tax-free income, particularly if it becomes a Modified Endowment Contract (MEC). Lastly, failing to analyze the specific economic conditions and interest rate environments projected for 2026 and beyond can lead to an inaccurate assessment of which vehicle will perform better for tax-free wealth accumulation, as each is sensitive to different market dynamics.

Ready to Build Your Financial Future?

Contact Everence Wealth for expert independent financial guidance.

Get in Touch