What common mistakes should pre-retirees avoid when planning for tax-free retirement income using indexed strategies?

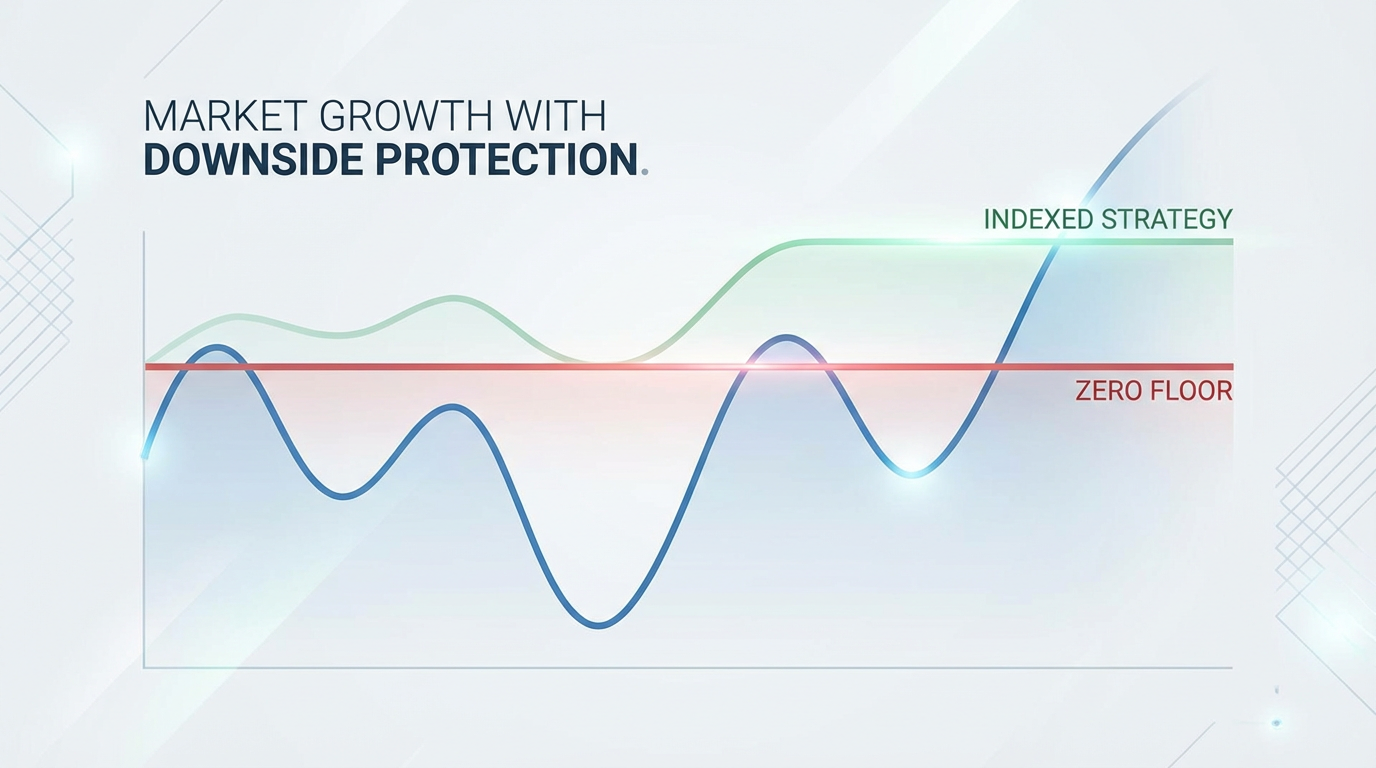

When pre-retirees plan for tax-free retirement income through indexed strategies, a significant pitfall is misunderstanding the cap rates and participation rates, which can lead to unrealistic return expectations. Another common mistake is failing to consider the impact of surrender charges and liquidity limitations, especially if access to funds is needed earlier than anticipated. Overlooking the importance of diversification is also a trap, as relying solely on one strategy, even an indexed one, might not align with a comprehensive financial plan. Finally, neglecting to review and adjust the strategy periodically based on changing market conditions or personal financial goals can undermine long-term success. ### Overlooking Cap and Participation Rates One of the primary pitfalls pre-retirees face with indexed strategies is not fully comprehending the implications of cap rates and participation rates. An indexed strategy links returns to a market index but often sets a maximum gain (cap rate) or a percentage of the index's growth (participation rate) that an investor can receive. Clients might focus solely on the 'no loss' feature and overlook how these caps or participation rates can limit their upside potential during strong market growth periods. This misunderstanding can lead to disappointment if actual returns do not meet initial, often exaggerated, expectations, highlighting the importance of understanding the balance between downside protection and upside limitation. ### Disregarding Liquidity and Surrender Charges Another common mistake involves underestimating the impact of surrender charges and liquidity constraints associated with many indexed products, such as fixed indexed annuities. These products are often designed for long-term growth, and accessing funds prematurely can trigger substantial fees, diminishing the overall value of the investment. Pre-retirees should carefully assess their potential need for early access to their capital and understand the surrender schedule before committing to such strategies. Failing to plan for unforeseen financial needs can turn a long-term benefit into a short-term financial burden. ### Neglecting Comprehensive Financial Planning and Diversification Focusing exclusively on indexed strategies for tax-free income without integrating them into a broader financial plan is a significant oversight. While indexed strategies offer distinct advantages, they should ideally complement a diversified portfolio that includes other asset classes and income streams. Relying too heavily on a single strategy, even a robust one, can expose an individual to concentration risk. A balanced approach ensures that various financial goals are addressed, and overall financial resilience is maintained, preventing over-reliance on any single investment vehicle for retirement income. It is crucial for pre-retirees to conduct thorough due diligence and engage with knowledgeable financial professionals who can clearly explain the intricacies of indexed strategies, including their benefits and limitations. Avoiding these common mistakes can significantly contribute to the successful implementation of a tax-free retirement income plan.

Ready to Build Your Financial Future?

Contact Everence Wealth for expert independent financial guidance.

Get in Touch